The increase in digital wallets, contactless payments and mobile money has continued since the COVID-19 pandemic, as consumers find them more convenient and practical compared to carrying a physical wallet. Equally Account to Account payments are fast emerging as an alternative to card payment rails.

So, what are digital wallets? Capital One defines them as “apps or online services that allow you to make transactions electronically”. Apple Pay, Google Pay, Alipay, PayPal and WeChat Pay are all types of digital wallets which can store information from a credit card, a debit card, coupons, and loyalty cards on a mobile device. The majority can be used both in-store and online. Recent data from Barclays shows the value of contactless payments in the UK has risen nearly 50% in 2022 with transactions above £100 increasing by 109%. Furthermore GSMA Newsroom, the industry organisation that represents the interests of mobile network operators worldwide, reports that between 2021 and 2022 total transaction value for mobile money increased by 22% globally.

What can we expect in UK payments going forward?

1. Who will provide the best digital wallet?

There will be a race to provide the best digital wallet as consumers are using digital wallets in an increasing variety of ways. Having a secure place for bank cards, coupons, loyalty cards or for holding an event ticket goes beyond sending money between contacts. Some mobile wallets are more complex, offering consumers the ability to maintain deposits, complete transactions, and to track expenses for budgeting and loyalty programmes. Adding features which use behavioural science informed prompts to promote saving or to limit spending on gambling is becoming more common. Improved and improving fraud prevention and protection will underpin these initiatives.

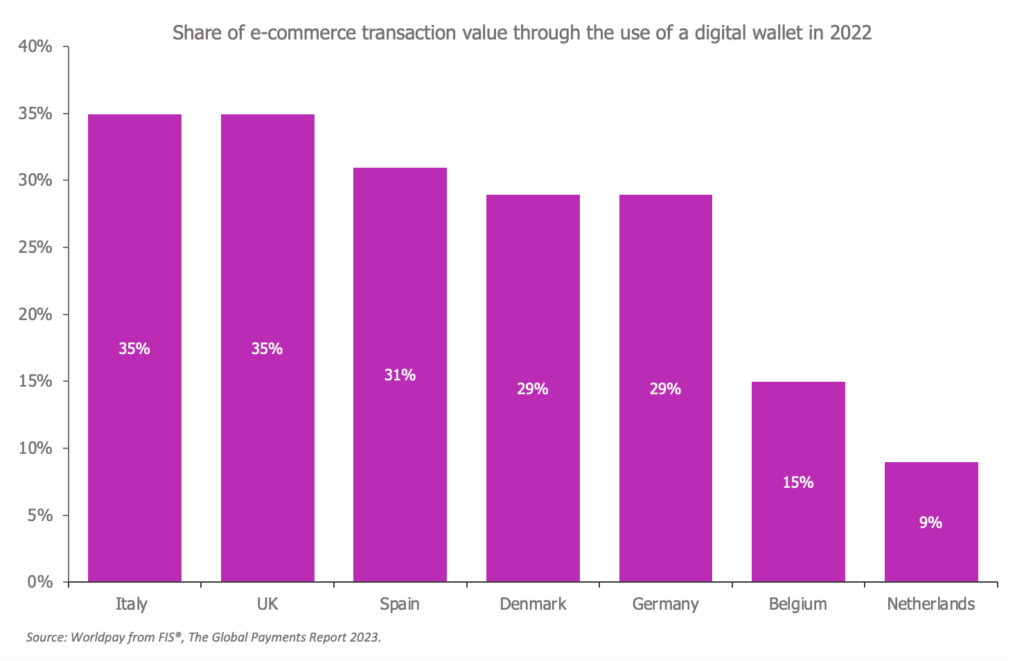

Globally in 2022 49% of transaction value for e-commerce payments and 32% of transaction value for point of sale payments were via a digital wallet according to Worldpay from FIS®, The Global Payments Report 2023.

Almost 10 years ago, our research report for Worldpay identified the emergence of ‘omnipayments’. At the time contactless payments were hardly used, but now consumers enjoy a plethora of payment methods. Winning the race to provide the best digital wallet is an important opportunity for payments providers, with the UK currently placed toward the front of the pack, in Europe at least.

2. How fast will Account to Account (A2A) payments grow?

A2A payments enable money to go directly from senders’ to receivers’ bank accounts, generally bypassing the card payment rail stage within the transaction. A2A payments are embedded in apps and online services such as Pix in Brazil and PromptPay in Thailand. These payments can occur between and among individual persons, businesses and governments.

There are a number of possible benefits of A2A payments including lower transaction costs for merchants compared to card payments, faster refunds and easier money management as transactions are instantly taken from bank accounts. Whether A2A payments will be more immune to fraud remains to be seen.

For A2A payments to increase substantially commentators suggest they need to be immediate, so that consumers can walk out of a store with their paid goods straightaway. However, replicating the immediacy of current in-store payment systems could be difficult, but with more and more services and products being bought online this is less of an obstacle.

A2A payments will be executed through senders’ and receivers’ accounts and managed through senders’ mobile banking apps or their online banking. Payments to a mobile number, email address or registered business name or business number, could minimize payment errors. We know from our research completed with Optal that human error is a big factor in payment inaccuracy although this process is protected by the intrinsic and rigorous security systems of banks.

But how long will it take for consumers to be made aware of the benefits of A2A payments and for them to change their payments’ habits? There could be many challenges for this payment method to grow including the familiarity and trust consumers hold for Visa and Mastercard. Consumers will need a strong incentive to make the switch to A2A payments as well as the conviction that this payment method is safe, secure and beneficial to them.

How will the UK fair in this new landscape? The Global Payments Report by WorldPay from FIS® suggests that A2A payments in Poland make up 67% of 2022 e-commerce transaction value, with the Netherlands at 62% and Finland at 34%. However, the UK shows only 5% of A2A payments for e-commerce transaction value in 2022 indicating a market with strong potential for growth.