Chris White and Marcus Hickman

Marketing science – especially as identified by industry authorities Byron Sharp and Jenny Romaniuk – shows that to really grow, a brand needs to be easier to access in consumer memory, in more buying situations, and for more consumers. It’s not just physical access that’s important but also mental access, and this involves building more than just brand awareness or positive attitudes towards a brand. The science suggests it is more important to create associations, refresh salience and build new memories so that a brand is chosen by consumers in a given situation, context or need state (“How to Grow Brands”, Sharpe). The 2020 Davies Hickman blog sets out the key principles of mental availability.

The building blocks of mental availability are Category Entry Point (CEPs) which are a combination of why a brand is demanded as well as the context within which it is demanded e.g. where, when, with whom? To increase and future-proof the share of the online market, brand executives need to know both the existing and the emerging entry points in the category, as well as whether the brand is strong or weak compared to competitors. In addition, it’s important to identify and plan responses to new opportunities and threats.

Chris White Consultancy and Davies Hickman Partners research methodologies enable executives to improve the mental availability of their brands. We assess the probability of customers thinking about brands in different buying situations when ordering online.

Applying mental availability to the home delivery market

Most consumers now order online for home delivery. In fact, our recent survey of 2,000 consumers confirms only 5% of UK consumers didn’t order online in November 2023.

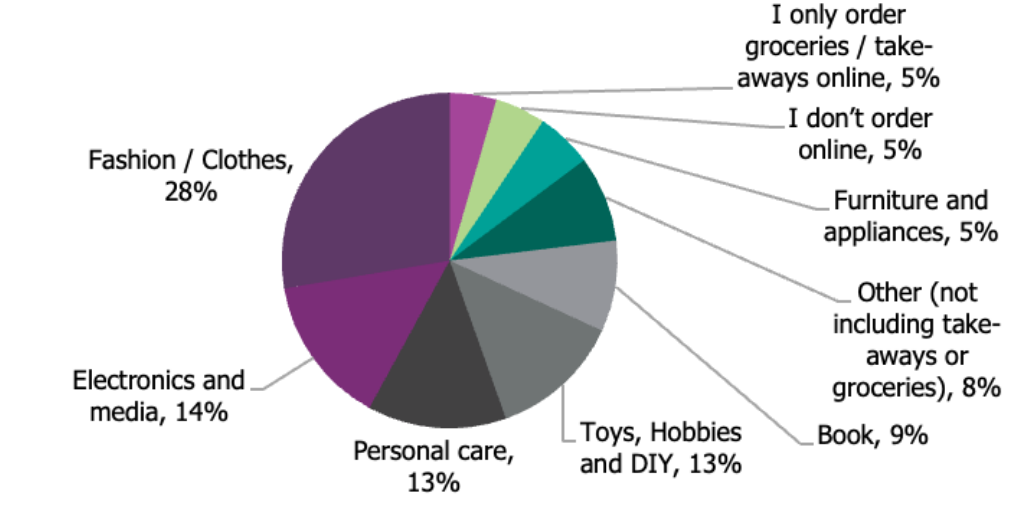

Figure 1 shows that Fashion, Electronics/Media, Personal Care, and Toy/Hobbies with DIY accounted for up to 70% of the market by value, with Fashion alone accounting for nearly a third of online orders. As Royal Mail continues to lose market share to other delivery providers, increasingly consumers are being offered a choice of who can deliver these products.

Figure 1 Online delivery by product type in the UK

Source: Chris White Consultancy/Davies Hickman Partners, 2024. UK 2,000 consumers nationally representative for age, gender and region.

The consumer context to online deliveries?

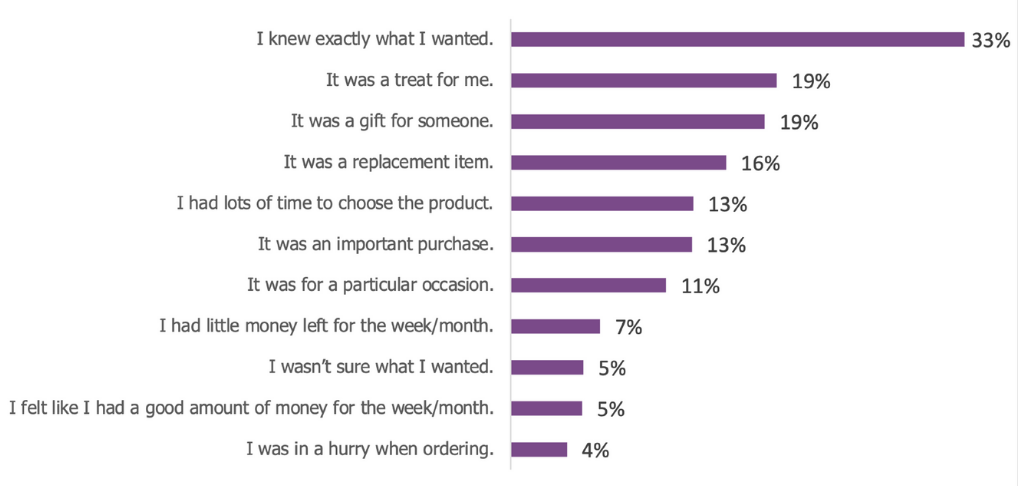

Our survey identifies the reasons consumers order online and the context of these orders. Figure 2 illustrates consumers’ contexts and it indicates that many orders are routine purchases with a third of consumers (33%) knowing exactly what they want and 15% making replacement purchases. Only 13% of consumers said the purchase is an important order, while a further 11% said their purchase was for a particular occasion. Perhaps counter to received wisdom, only 4% suggested they were in a hurry when ordering while three times as many were purchasing when they had no time constraint (13%).

Figure 2 Consumer context when ordering an online delivery % Select all that apply

Source: Chris White Consultancy/Davies Hickman Partners, 2024. UK 2,000 consumers nationally representative for age, gender and region.

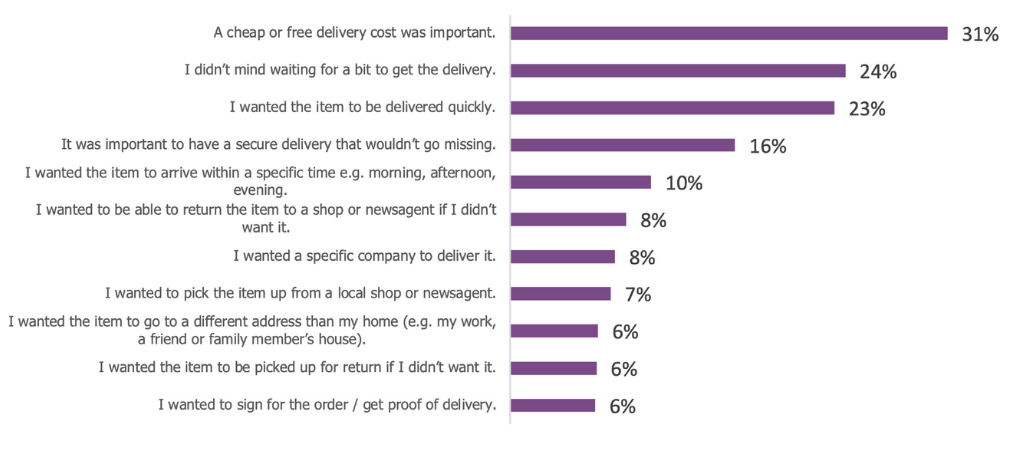

In Figure 3, the needs for online delivery show the importance of routine orders. Some 31% of consumers are wanting a free or low-cost delivery and 24% of consumers do not mind waiting for a delivery. There are over 10 online delivery needs that can be satisfied by differing offers.

Figure 3 Consumer need when ordering an online delivery % agreeing

Source: Chris White Consultancy/Davies Hickman Partners, 2024. UK 2,000 consumers nationally representative for age, gender and region.

Understanding the Category Entry Points (CEPs) for home delivery

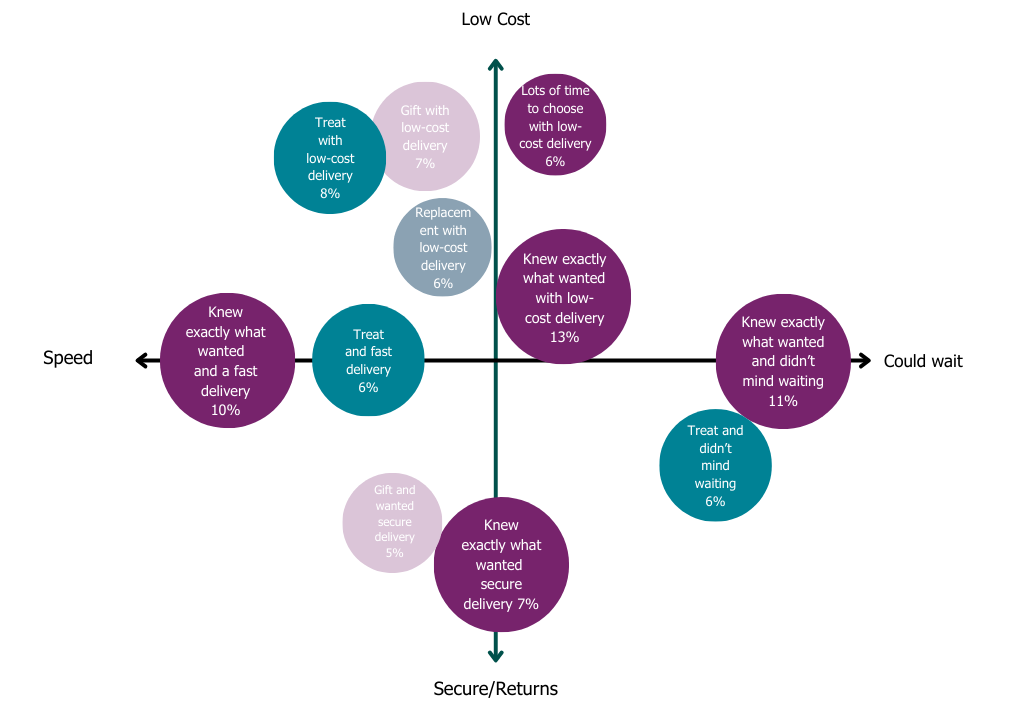

Deeper consumer insight can be achieved by analysing the crossover between consumer needs and consumer contexts at the point of ordering and therefore identifying key CEPs for online delivery.

Figure 4 Category Entry Points for online deliveries

Source: Chris White Consultancy/Davies Hickman Partners, 2024. UK 2,000 consumers nationally representative for age, gender and region.

Figure 4 illustrates the top 11 CEPs for consumers ordering goods online (excluding grocery and takeaways). The key groups are focussed towards low cost (40% of the market), speed (16%), no time constraint (17%) and those consumers who are concerned about security and returns (16%). While low cost is the largest group and includes a range of contexts, there are other important combinations. For example, those ordering gifts and those knowing what they want may also have a high need for secure signing or return options. Interestingly while some of those ordering treats were often happy to wait longer for delivery (6%) an equal number wanted the treats quickly (6%). The largest group of consumers, those who knew exactly what they wanted when ordering, had a variety of different needs with price, speedy delivery, as well as no time constraint and security/returns all being important CEPs.

How to grow your online delivery brand by understanding your CEP strengths (and weaknesses)

Chris White Consultancy and Davies Hickman can help online delivery companies and retailers grow their brands by understanding how their and their competitors’ brands are performing against CEPs. This understanding will help retailers direct product and service improvements, marketing and communication spend in the marketplace, and relationships with online retailers.

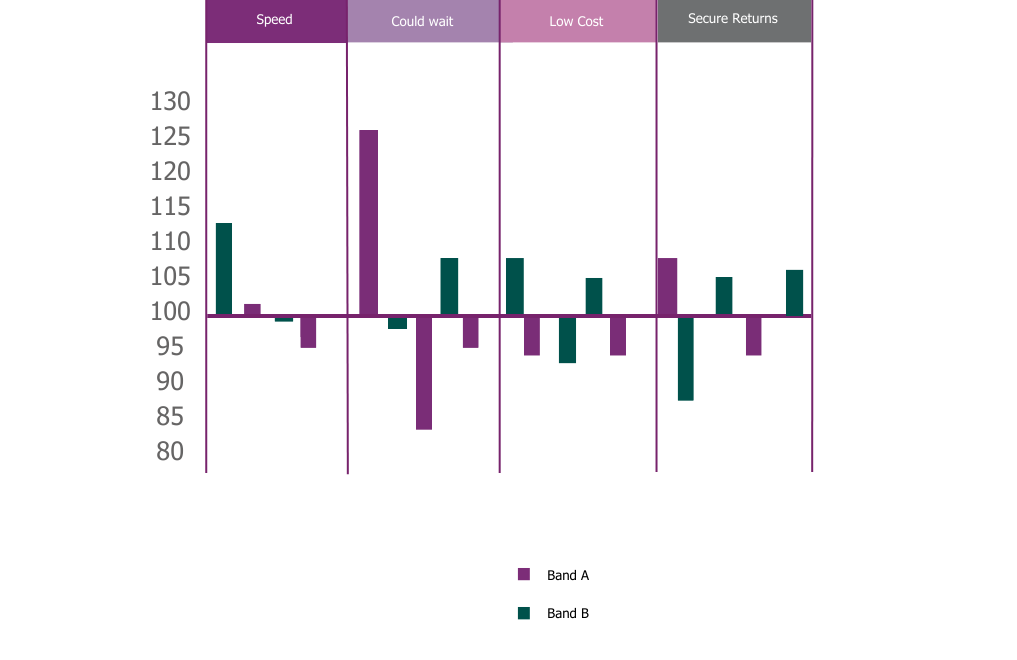

Figure 5 shows a comparison of two brands’ mental availability indexed against the brands’ average performance to show their relative strengths and weaknesses in the market. The analysis shows that Brand B was better in CEP’s around Speed and Low Cost, with Brand A being better around CEP’s where consumers didn’t mind wating. These findings can really help brands fine tune their marcomms messaging and media targets to be available in as many CEP’s as possible.

Figure 5 A comparison of mental availability between brands

Source: Chris White Consultancy/Davies Hickman Partners, 2024. UK 2,000 consumers nationally representative for age, gender and region.

An understanding of the key CEPs in a market, and the mental availability of a brand compared to the competition, offers a powerful insight to measure the effectiveness of ongoing campaigns and provides a strategic tool to plan brand marketing. Study after study has shown that the higher a brand’s share of Category Entry Points, the larger its market share. Indeed this data provides a much more reliable indicator of market share than overall spontaneous awareness figures.